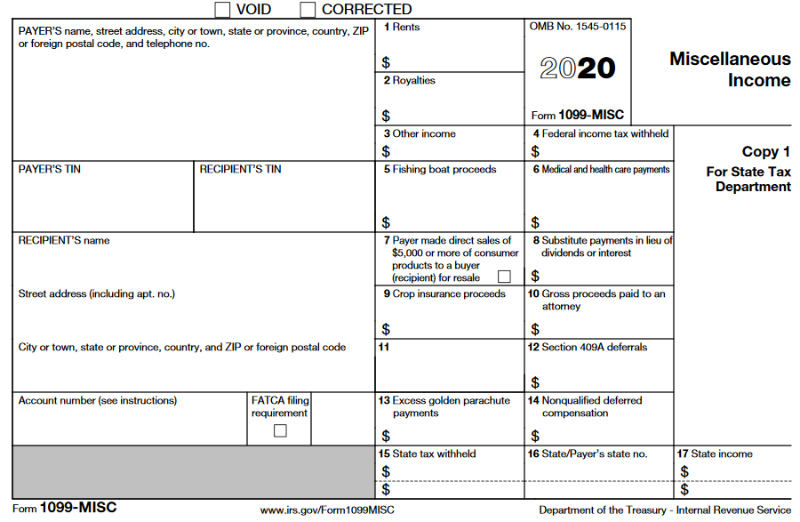

Non-Employee Compensation is no longer reported on the 1099 MISC form. All information reported in Box 7 in previous years must be reported on the NEW 1099 NEC form.

File a Form 1099-MISC, Miscellaneous Income, for each person in the course of your business to whom you have paid the following during the year:

At least $10 in royalties and at least $600 in rents, prizes and awards, other income, fishing boat proceeds, health care payments, crop insurance proceeds, attorney proceeds, section 409A deferrals, or nonqualified deferred compensation.

Due to the creation of Form 1099-NEC, the IRS has revised Form 1099-MISC and rearranged box numbers for reporting certain income. Changes in the reporting of income and the form’s box numbers are listed below.